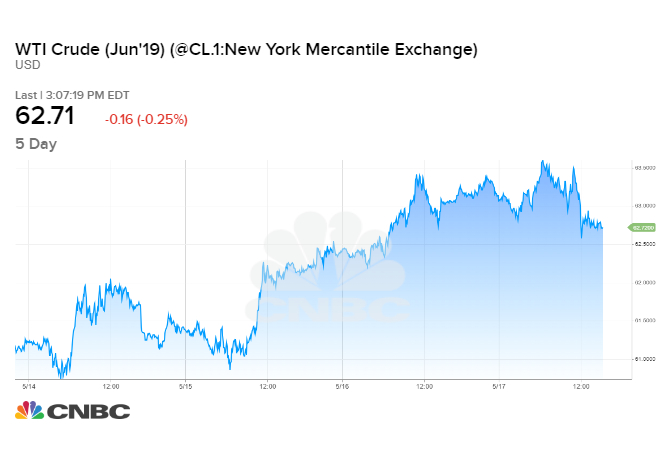

Oil prices have risen about 2% this week on Middle East tensions. If the rhetoric from Washington cools, oil prices could pull back at least $2 a barrel, Kilduff said.

President Trump’s fear of Joe Biden seems well-founded, especially since Biden is now favored to move into the White House in 2021, by some estimates. “With Trump facing an unlikely reelection, this means it is most likely at this point Joe Biden will win the general election in November,” Washington, DC research firm Sandhill Strategies predicted in a March 16 analysis. The coronavirus outbreak has triggered a bear market in stocks and a likely recession , which is a death sentence for presidential reelection hopes. “No U.S. President has won reelection in recent history after a period of economic downturn,” Sandhill points out. Biden hasn’t officially clinched the Democratic presidential nomination yet. But that seems inevitable, barring an unforeseen turn in the race. He handily leads Bernie Sanders in the delegate count , and Sanders himself seems to be tacitly acknowledging his inevitable dropout. Recessions are funny things, because economists only declare them months afte...

Recently fast grew by European and then Japanese and South Korean help, the automotive industry in Turkey plays an important role in the manufacturing sector of the Turkish economy. The foundations of the industry was laid with the establishment of Otosan assembly factory in 1959 and the mass production of the domestic car Anadol in 1961. Last years Turkey produced up to 1.2 million motor vehicles, ranking as the 7th in Europe and the 16th-17th largest producer in the World. With a cluster of car-makers and parts suppliers, the Turkish automotive sector has become an integral part of the global network of production bases, exporting over $22,944,000,000 worth of motor vehicles and components in 2008. Global car manufacturers with production plants include Mercedes-Benz , Fiat / Tofaş , Oyak-Renault , Hyundai , Toyota , Honda and Ford / Otosan .

Figure 1. World oil (crude and condensate) average daily production and refiners average acquisition cost in 2009 $, both based on EIA data. 2010 is partial year through September 30. /// /// /// . Figure 2. Graph of Persian Gulf oil (crude and condensate) based on EIA data. /// . Figure 3. Persian Gulf oil production and average price, based on EIA data. /// . Figure 4. OPEC reserves based on BP Statistical Report data. Graph by Rune Likvern of The Oil Drum. /// : Figure 5. Oil production from the Former Soviet Union, based on EIA data (crude and condensate). /// The USA: Figure 6. US (crude and condensate) oil production, based on EIA data. /// : Figure 8. Oil production (crude and condensate) for the rest of the world based on EIA data. /// International International energy data and analysis /// International Energy Outlook 2014 /// World markets for petroleum and other liquid fuels have entered a p...

Comments

Post a Comment